Questions for the future Nowadays, almost all of our everyday goods are shipped in ocean containers. The maritime container trade market had been growing exponentially before it was hit by the 2008 financial crisis, when global GDP growth lost power to drive maritime container trade growth. In addition, the rise of protectionist trade and the introduction of so-called Fourth Industrial Revolution technologies, such as robotics and 3D printing technology, are changing the maritime container trade market.

On top of that, the container shipping industry is undergoing major changes, including ships becoming larger in size, digital transformation of shipping transactions and contracts, e-commerce companies entering the logistics industry, vertical integration of shipping companies, social demands for eco-friendly maritime transportation, and the Panama Canal drought caused by climate change.

On this note, we are faced with the following two questions:

1) What are the survival strategies for the container shipping industry in the future?

2) Can digital transformation and formation of a predictable supply chain serve as a survival strategy for the container shipping industry? How the container shipping industry has evolved Over the past 50 years, the container shipping industry has grown tremendously. The growth of container shipping has increased the share of international trade in global GDP to 25% in 2022.[1] This was largely driven by Japan, which has adopted an export-led growth strategy, as well as late-comers such as South Korea, China, and Taiwan. China's accession to the WTO in 2001 was also significant for the global economy. It marked the integration of China into the global economy and brought a huge labor force into the global economy. With China's WTO accession, many countries decided to offshore to China, signaling the formation of the global value chain.

Amid the wave of international trade growth, there were instances where cargoes that were once classified as purely bulk cargo were shipped in containers, which was partially due to the advantages of containers. The benefits of containers, which can be summarized as modularity, simplicity, resistance to pilferage, and efficiency, were indeed appealing to shippers. As a result, around 165 million TEUs were traded in containers globally in 2021, which was a quantum leap from 1968, when less than 1 million TEUs of cargo were traded in containers globally.[2]

On top of that, the container shipping industry is undergoing major changes, including ships becoming larger in size, digital transformation of shipping transactions and contracts, e-commerce companies entering the logistics industry, vertical integration of shipping companies, social demands for eco-friendly maritime transportation, and the Panama Canal drought caused by climate change.

On this note, we are faced with the following two questions:

1) What are the survival strategies for the container shipping industry in the future?

2) Can digital transformation and formation of a predictable supply chain serve as a survival strategy for the container shipping industry? How the container shipping industry has evolved Over the past 50 years, the container shipping industry has grown tremendously. The growth of container shipping has increased the share of international trade in global GDP to 25% in 2022.[1] This was largely driven by Japan, which has adopted an export-led growth strategy, as well as late-comers such as South Korea, China, and Taiwan. China's accession to the WTO in 2001 was also significant for the global economy. It marked the integration of China into the global economy and brought a huge labor force into the global economy. With China's WTO accession, many countries decided to offshore to China, signaling the formation of the global value chain.

Amid the wave of international trade growth, there were instances where cargoes that were once classified as purely bulk cargo were shipped in containers, which was partially due to the advantages of containers. The benefits of containers, which can be summarized as modularity, simplicity, resistance to pilferage, and efficiency, were indeed appealing to shippers. As a result, around 165 million TEUs were traded in containers globally in 2021, which was a quantum leap from 1968, when less than 1 million TEUs of cargo were traded in containers globally.[2]

(Source : Getty Images Bank)

(Source : Getty Images Bank) In the early days of containerized ships, the largest ships were 1,000 TEU-class vessels. However, in 1966, McKinsey claimed that container ships would follow the trend of tankers becoming larger in size and predicted the emergence of 10,000 TEU ships. As of 2023, the largest container ship today is MSC's 24,236 TEU-class vessel. However, containerization has created an oversupply of ships which sparked mergers and acquisitions among shipping lines. The advent of containers has also created an oligopolistic shipping market. In 1995, the top five shipping lines accounted for only 27% of the market, but by 2023, they accounted for a whopping 64.5% of the entire market.[3]

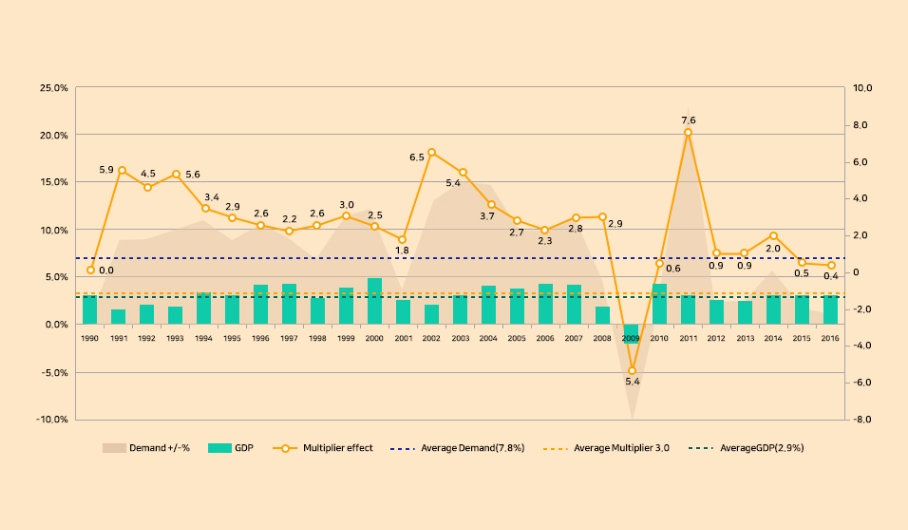

Consequences of the global financial crisis The global financial crisis of 2008-2009 was an inflection point for the container shipping industry. In the decade prior to 2009, global trade growth had doubled or tripled global GDP growth. In addition, global trade growth had never slowed down before 2009. However, with the slowdown of globalization, global trade growth showed similar figures with global GDP growth.

Consequences of the global financial crisis The global financial crisis of 2008-2009 was an inflection point for the container shipping industry. In the decade prior to 2009, global trade growth had doubled or tripled global GDP growth. In addition, global trade growth had never slowed down before 2009. However, with the slowdown of globalization, global trade growth showed similar figures with global GDP growth.

[Multiplier effect between global GDP and international trade]  (Source: IMF & KMI[4])

(Source: IMF & KMI[4])

(Source: IMF & KMI[4]) The global financial crisis has created other problems as well. Inequality has exacerbated in many parts of the world, and unemployment, low wages, and job loss due to automation have emerged as serious social problems. In addition, doubts about the sustainability of the Chinese economic model rose to the surface. In 2019, the entire world was hit by the COVID-19 outbreak in Wuhan, China, and skepticism about globalization, which is closely linked to global value chains that rely on China, gained momentum. What will happen to the container shipping industry? 1) Peak Container?

It is evident that globalization, the industrialization of Asia’s emerging economies, and containerization will not be valid for container trade growth for good. Furthermore, the container shipping industry is faced with the question of how robotics, automation, and 3D printing will change consumption patterns and streamline global value chains.

Previously, globalization has been largely driven by free trade policies, the proliferation of global value chains, and the influx of one billion Chinese workers into the global economy. However, recent trends of free trade have shifted from multilateral agreements led by the WTO to "smaller," "bilateral," and "plurilateral" agreements. Since 2011, the proliferation of global value chain has slowed down, and China's labor force is shrinking while wages are rising.

All these trends seem to point out that demand for containerized ocean trade has reached its peak. Nevertheless, China's Belt and Road policy that have been implemented since 2015 has been a boon for globalization.

It is evident that globalization, the industrialization of Asia’s emerging economies, and containerization will not be valid for container trade growth for good. Furthermore, the container shipping industry is faced with the question of how robotics, automation, and 3D printing will change consumption patterns and streamline global value chains.

Previously, globalization has been largely driven by free trade policies, the proliferation of global value chains, and the influx of one billion Chinese workers into the global economy. However, recent trends of free trade have shifted from multilateral agreements led by the WTO to "smaller," "bilateral," and "plurilateral" agreements. Since 2011, the proliferation of global value chain has slowed down, and China's labor force is shrinking while wages are rising.

All these trends seem to point out that demand for containerized ocean trade has reached its peak. Nevertheless, China's Belt and Road policy that have been implemented since 2015 has been a boon for globalization.

[China's share of processed trade and growth in intermediate goods imports]  (Source: Bank of Korea[5])

(Source: Bank of Korea[5])

(Source: Bank of Korea[5]) Industrialization in Asia's emerging economies led by China and India is still underway. India, in particular, is trying to decide which of the policy recipes to follow - tax, labor market, land reform, infrastructure investment, business deregulation, and productivity growth. One thing is for sure: India is emulating 'Made in China' to spread 'Make in India' around the globe.

2) LCL containers meet digital

Global container trade has grown from 40 million TEUs in 1996 to 160 million TEUs in 2022 (Review of Maritime Transport 2023, UNCTAD). However, under-utilization of container boxes has led to a steady decline in stuffing trade. There is no shortage of container boxes per se, as the shipment sizes for containerized trade are getting smaller and smaller. Therefore, there is a growing need for a "conveyor belt-like container box supply chain" from factory to consumer. A container box supply chain with greater visibility and predictability will also improve cargo traceability.

The trend of decline in stuffing will create new business opportunities for through transport operators who use the same vehicle for each transportation section. For example, containers departed from China are mixed at the CFS near the port, with 90% of them arriving in LA/LB ports. Half of the cargo arriving in LA/LB ports is mixed into other containers in the port area. In addition, most of Indonesia's containerized imports is unpacked in the port area and transported inland by truck. If improved analytics and self-driving trucks are introduced, it will be highly useful for through transport operators and will make transportation simpler and cheaper.[6]

2) LCL containers meet digital

Global container trade has grown from 40 million TEUs in 1996 to 160 million TEUs in 2022 (Review of Maritime Transport 2023, UNCTAD). However, under-utilization of container boxes has led to a steady decline in stuffing trade. There is no shortage of container boxes per se, as the shipment sizes for containerized trade are getting smaller and smaller. Therefore, there is a growing need for a "conveyor belt-like container box supply chain" from factory to consumer. A container box supply chain with greater visibility and predictability will also improve cargo traceability.

The trend of decline in stuffing will create new business opportunities for through transport operators who use the same vehicle for each transportation section. For example, containers departed from China are mixed at the CFS near the port, with 90% of them arriving in LA/LB ports. Half of the cargo arriving in LA/LB ports is mixed into other containers in the port area. In addition, most of Indonesia's containerized imports is unpacked in the port area and transported inland by truck. If improved analytics and self-driving trucks are introduced, it will be highly useful for through transport operators and will make transportation simpler and cheaper.[6]

(Source : Getty Images Bank)

(Source : Getty Images Bank) 3) Robotics and 3D printing

There are many factors at play in determining where a product is manufactured besides low labor costs. For example, automobiles are manufactured in various locations due to high transportation and customs costs, as well as the need for customization that caters to local preferences. Petrochemical products are also manufactured where there is access to raw materials and low energy prices. It is estimated that 10-15% TEU of total trade volumes is produced in regions with low labor costs.[6] Therefore, the argument that the introduction of robotics will increase nearshoring (i.e., outsourcing production to a country in proximity to advanced economies) is indeed short-sighted.

The adoption of 3D printing technology raises deeper questions about containerized transportation. 3D printing will bring production closer to the consumer than it is now, which may even create a "homegrown 3D printing industry" from offshoring, nearshoring, to reshoring. At the current speed of development, however, 3D printing will be a "slow and expensive option" for most of the product production. Accordingly, the maturity of 3D printing technology will determine the future trade patterns.

4) Change of consumption patterns

With the development of digitalization, our consumption patterns are also changing from "goods consumption" to "service consumption". For example, digital products such as e-books instead of physical goods are increasingly becoming popular gifts at Christmas. Many parents are also buying game money instead of toys for their children's birthdays.

Meanwhile, e-commerce companies are responding to customer orders with greater speed and reliability. The fidget toy shortages of summer 2017 as illustrated below clearly showed mounting consumer dissatisfaction caused by slow lead time of multinational supply chains. [7] Fidget toy and shipping liners In 2017, there was a wake-up call in the shipping and logistics industry. As the craze for small toys called “fidget toys” in Europe had outstripped all expectations, retailers decided to ship them by air transportation. This incident dispelled the long-standing belief that airfreight cargo should consist of expensive goods and raised the alarm for the shipping companies that boldly continued the practice of blank sailing or slow steaming.

There are many factors at play in determining where a product is manufactured besides low labor costs. For example, automobiles are manufactured in various locations due to high transportation and customs costs, as well as the need for customization that caters to local preferences. Petrochemical products are also manufactured where there is access to raw materials and low energy prices. It is estimated that 10-15% TEU of total trade volumes is produced in regions with low labor costs.[6] Therefore, the argument that the introduction of robotics will increase nearshoring (i.e., outsourcing production to a country in proximity to advanced economies) is indeed short-sighted.

The adoption of 3D printing technology raises deeper questions about containerized transportation. 3D printing will bring production closer to the consumer than it is now, which may even create a "homegrown 3D printing industry" from offshoring, nearshoring, to reshoring. At the current speed of development, however, 3D printing will be a "slow and expensive option" for most of the product production. Accordingly, the maturity of 3D printing technology will determine the future trade patterns.

4) Change of consumption patterns

With the development of digitalization, our consumption patterns are also changing from "goods consumption" to "service consumption". For example, digital products such as e-books instead of physical goods are increasingly becoming popular gifts at Christmas. Many parents are also buying game money instead of toys for their children's birthdays.

Meanwhile, e-commerce companies are responding to customer orders with greater speed and reliability. The fidget toy shortages of summer 2017 as illustrated below clearly showed mounting consumer dissatisfaction caused by slow lead time of multinational supply chains. [7] Fidget toy and shipping liners In 2017, there was a wake-up call in the shipping and logistics industry. As the craze for small toys called “fidget toys” in Europe had outstripped all expectations, retailers decided to ship them by air transportation. This incident dispelled the long-standing belief that airfreight cargo should consist of expensive goods and raised the alarm for the shipping companies that boldly continued the practice of blank sailing or slow steaming.

[Fidget toys]

2030 Future Strategy for Container Shipping Logistics As shown above, the container trade market has both good and bad news. It is undeniable that the container shipping industry faces a big challenge ahead of it: digital transformation. Then, how should we prepare for the future? One thing is evident: digital will not change the physical nature of shipping. Even the most automated smart port will not change the role of cranes lifting cargo and placing it on land or on board. The idea that underwater hyperloops will replace ships in the future is nothing more than a science fiction.

1) Focus on the real end customer

While the customer of the container shipping industry was just Walmart in the past, the future container shipping customer will be the end consumer who buys goods from Walmart. Therefore, it is imperative to listen to their needs and serve their interests.

2) Keep a close eye on (monitor) triggers

Keep a close eye on infrastructure investment, labor costs per unit, e-commerce adoption by SMEs, 3D printing adoption and dynamics, how much funding container shipping startups have received from venture capitalists, the size of the latest mega-ships ordered, and the speed of digital platform adoption.

3) Go digital from the ground up

Lastly, enable, automate and innovate predictive maintenance, smart stowage, seamless document flow, and omniscient cargo tracking. # Reference [1] : European Commission, 2023

[2] : New Maritime Powerhouse: The Future of the Korean Shipping Industry, PwC Korea, 2023

[3] : Worldwide; Alphaliner; September 30, 2023

[4] : IMF & KMI, ‘Global Economic Trends’ & Drewry, ‘Container Market Review and Forecaster 3Q 2016’

[5] : The Bank of Korea, Background and Implications of Weakening Linkages Between Global Growth and Trade, Global Economic Review (2019.4.18)

[6] : Brave new world? Container transport in 2043, Mckinsey&Company 2019

[7] : Financial Times, 2017, https://www.ft.com/content/5ead667c-3c0a-11e7-821a-6027b8a20f23

▶ This content is protected by the Copyright Act, and the copyright is held by the contributor.

▶ This content is prohibited from secondary processing and commercial use without prior consent.

1) Focus on the real end customer

While the customer of the container shipping industry was just Walmart in the past, the future container shipping customer will be the end consumer who buys goods from Walmart. Therefore, it is imperative to listen to their needs and serve their interests.

2) Keep a close eye on (monitor) triggers

Keep a close eye on infrastructure investment, labor costs per unit, e-commerce adoption by SMEs, 3D printing adoption and dynamics, how much funding container shipping startups have received from venture capitalists, the size of the latest mega-ships ordered, and the speed of digital platform adoption.

3) Go digital from the ground up

Lastly, enable, automate and innovate predictive maintenance, smart stowage, seamless document flow, and omniscient cargo tracking. # Reference [1] : European Commission, 2023

[2] : New Maritime Powerhouse: The Future of the Korean Shipping Industry, PwC Korea, 2023

[3] : Worldwide; Alphaliner; September 30, 2023

[4] : IMF & KMI, ‘Global Economic Trends’ & Drewry, ‘Container Market Review and Forecaster 3Q 2016’

[5] : The Bank of Korea, Background and Implications of Weakening Linkages Between Global Growth and Trade, Global Economic Review (2019.4.18)

[6] : Brave new world? Container transport in 2043, Mckinsey&Company 2019

[7] : Financial Times, 2017, https://www.ft.com/content/5ead667c-3c0a-11e7-821a-6027b8a20f23

▶ This content is protected by the Copyright Act, and the copyright is held by the contributor.

▶ This content is prohibited from secondary processing and commercial use without prior consent.